Short answer: the BWA is raw material for steering

A BWA shows interim revenue, cost and profit development in a German business. It does not replace cash-flow planning or management interpretation. For managing directors, CFOs and international parent companies, it becomes valuable when it is timely, checked, explained and connected to action.

What do you want to do with your BWA?

Start with DATEV reporting if your monthly BWA should become a repeatable management process. The other paths help when you first want to read, check or validate individual BWA signals.

Automate DATEV reporting

Turn recurring BWA, SuSa and AR/AP exports into a management report with KPI logic, plausibility checks and commentary.

Read and understand the BWA

A practical 10-minute sequence for revenue, gross profit, costs, result and plausibility.

Start the BWA Quick Check

Interpret your own KPIs, identify warning signs and decide what to review next.

Check BWA with SuSa

Use account-level detail, open items and accruals to validate BWA signals.

How to Read a German BWA as a Management Report

A practical guide for managing directors, CFOs and controllers: compare trends and margins, test result quality, connect account detail, open items and liquidity, and assign the next action.

The BWA, briefly explained

A BWA is an interim business evaluation based on financial accounting data. It shows how revenue, costs, gross margin and profit develop during the financial year. In many German companies, it is created monthly by the tax adviser, accounting team or finance system.

It typically helps answer: What revenue was recorded this month and year to date? How are materials, purchased services and gross margin developing? Which cost categories are increasing? What is the preliminary result? Which movements should management investigate?

Important: a BWA is not a statutory annual financial statement, not a complete cash-flow report and not a substitute for management interpretation. It becomes decision-relevant only when it is explained, compared, challenged and connected to additional information.

Understanding a BWA: which KPIs really matter

The BWA condenses current bookkeeping data into a financial snapshot of a German business. It mainly shows profitability: which revenue or output was recorded, which costs were incurred and which preliminary result remains.

The exact format can vary depending on the business, chart of accounts, tax adviser, accounting system and reporting setup. For management, the most important question is not whether every line can be explained technically. The more important question is whether the BWA creates the right management questions: Is growth profitable? Is gross margin strong enough? Are personnel costs and overheads plausible? Are there signs of liquidity, margin or financing issues? If you first need a quick reading sequence, use the practical guide How to read a German BWA report.

The BWA is often over-trusted and underused

“The BWA is not the final product. It is the raw material for management reporting.”

The most dangerous BWA misunderstandings

Many questions from banks, boards and shareholders are not caused by poor numbers, but by numbers that have not been put into context.

| Misunderstanding | Why it is risky | Better management view |

|---|---|---|

| The BWA shows our liquidity. | The BWA is primarily profit-oriented. Payment terms, receivables, payables, taxes, investments and loans are only partly visible. | Read profit and liquidity separately and connect the BWA with open-item lists, bank accounts, working capital and liquidity planning. |

| If the BWA comes from DATEV, it is automatically management-ready. | DATEV exports provide a data basis, but management relevance requires timing, comparison, commentary and action logic. | Use BWA and DATEV data as the basis for a decision-oriented monthly report. |

| The tax adviser report replaces internal reporting. | Tax adviser reports are often accounting- or tax-driven. Management needs an additional decision layer. | Add a management reporting layer on top of bookkeeping and tax reporting. |

| A positive BWA is enough for the bank. | Banks often want plausibility, SuSa detail, open-item lists, annual accounts, liquidity view, forecast and explanations. | Prepare the BWA with commentary and supporting documents. |

| SuSa is only accounting detail. | Without account-level detail, many BWA deviations remain too aggregated. | Use the SuSa as the bridge from summary line to root cause. |

Why many BWA reports fail as management tools

A BWA can be technically correct and still fail as a management instrument. This happens when it is treated only as an accounting output.

Common gaps include late availability, missing accruals, missing inventory movements, unclear one-off effects, missing budget or prior-year comparisons, no SuSa drill-down and no follow-up on actions.

This becomes critical when the BWA is forwarded to banks, shareholders or advisory boards without explanation. Acceptable numbers do not automatically create confidence if commentary, forecast and actions are missing.

BWA structure: which lines matter in a management-ready report

Revenue and total operating performance show which output was recorded in the reporting period. For management, the absolute figure alone is not enough: growth is positive only if margin, cash flow, capacity and earnings quality develop with it.

Materials, purchased goods and external services become relevant when read in relation to output. If revenue increases but gross margin falls, this can indicate price pressure, project issues, purchasing effects, discounts, product mix or accounting classification issues.

Gross margin is a central steering indicator. It shows what remains after direct costs to cover personnel, overheads, financing, investment and profit.

Personnel costs should be read in relation to revenue, gross margin, utilisation, productivity and organisational development. Other operating expenses often reveal cost drift. Operating result and preliminary result finally show whether earnings quality is operationally earned or driven by one-offs.

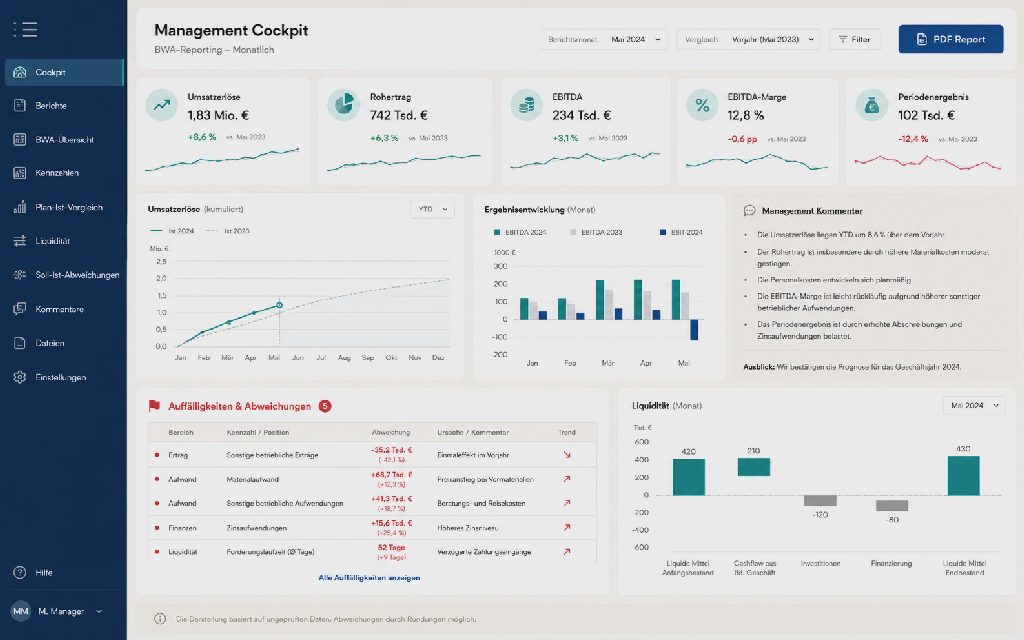

Accessible description and data

The infographic structures a German BWA review into five signals: revenue development, gross profit and margin, cost blocks, earnings quality and plausibility with SuSa, AR/AP and liquidity.

BWA red flags management should take seriously

| Signal in the BWA | Why it matters | First management question |

|---|---|---|

| Revenue increases, gross margin decreases | Growth may be unprofitable. | Are we selling more, but worse? |

| Profit is positive, liquidity is tight | Profit does not equal available cash. | Are receivables, stock, projects, taxes or debt service absorbing cash? |

| Personnel costs rise faster than performance | Capacity build-up can weigh on profit and cash flow. | Are pipeline, utilisation and margin supporting the cost base? |

| Strong monthly swings | Accounting timing or one-offs can hide the real trend. | Is this operational or a periodisation issue? |

| No SuSa drill-down | Summary lines remain insufficiently explainable. | Which accounts explain the deviation? |

| No commentary | Stakeholders must interpret the numbers themselves. | What story do the numbers tell, and what action follows? |

BWA and SuSa: why the BWA alone is often not enough

The strength does not come from one document alone. It comes from connecting the right reports.

| Report | What it shows | How it helps | Limit |

|---|---|---|---|

| BWA | Aggregated under-year profit development | Monthly steering, trends, deviations, bank communication | Too aggregated for root causes and liquidity |

| SuSa | Account-level balances and movements | Root-cause analysis, plausibility checks, detailed explanation | Often too technical without management translation |

| Open-item list | Open receivables and payables | Liquidity, working capital, payment risks | Does not show earnings quality by itself |

| Liquidity forecast | Expected cash inflows and outflows | Solvency, funding need, debt service | Depends strongly on assumptions and update discipline |

| Annual accounts | Formal financial statement for the financial year | Historical assessment, financing, transactions, tax context | Often too late for ongoing management |

What banks, investors and advisory boards really want from a BWA

For banks, investors and advisory boards, the BWA is rarely just a spreadsheet. It is a plausibility check of the current business development.

Typical questions include: Is the company developing steadily? Are revenue, gross margin and profit explainable? Are there one-off effects? Is liquidity sufficient? Do earnings, debt service and financing structure fit together? Does management identify deviations early?

Bank-ready does not necessarily mean a different BWA. It means a BWA that is timely, explainable, reconcilable and connected to management action. A useful reporting package therefore combines BWA, SuSa, open items, a short liquidity view, relevant commentary, forecast and open actions.

Analyze DATEV BWA exports: from tax-adviser report to monthly management report

The classic BWA is created from financial accounting, often as a DATEV or tax-adviser export. A management report starts with a different question: Which decisions do we need to make based on these numbers?

A good monthly management report adds clear KPI selection, prior-year and budget comparison, explanation of material deviations, liquidity and working-capital perspective, forecast, actions, responsibilities and concise management commentary.

The value is not in making the BWA look nicer. The value is in translating numbers into management. If BWA, trial balance and open-item exports should become a recurring workflow, DATEV BWA Reporting is the right next step.

Five practical patterns we often see

Profitable on paper, tight on cash

The BWA shows profit, but receivables, stock, projects or taxes absorb cash. Profit, open items, working capital and forecast must be read together.

Growth hides margin erosion

Revenue increases while gross margin falls. Project margins, discounts, purchasing costs or product mix reduce earnings quality.

The BWA fluctuates more than the business

Missing accruals, inventory logic or irregular postings distort monthly results and lead to poor conclusions.

The bank receives numbers, but no story

Uncommented numbers create questions. Good preparation connects BWA, forecast, liquidity bridge and explanation of special effects.

DATEV exports become a management cockpit

Recurring KPI logic, commentary fields, variance analysis and action tracking make existing data management-ready.

The Momentum perspective: BWA as a steering and value-creation instrument

Momentum Advisory does not look at BWA, DATEV exports and finance data in isolation. The important question is whether they lead to better decisions, less manual work, more transparency and a measurable contribution to enterprise value.

A BWA becomes especially valuable when it is connected to three layers: interpretation, steering and scaling. This is relevant for companies that are growing, raising finance, investing, restructuring, preparing for succession or seeking to increase enterprise value.

Our focus is not to replace bookkeeping, tax advisers or annual accounts. The goal is to make existing finance data management-ready based on provided BWA, SuSa, open-item or DATEV exports.

Five steps: how to turn a BWA into a decision basis

The BWA becomes valuable when the process becomes repeatable: from data quality to action logic.

Check data quality and timing

Review whether bookings are complete, current and allocated to the right period. Pay attention to accruals, inventory movements and late postings.

Read the BWA relatively

A single monthly value says little. Meaning comes from previous month, previous year, budget, forecast and ratios.

Investigate unusual positions with SuSa

If a BWA line looks unusual, trace it to account level.

Add management commentary

Relevant deviations should briefly explain what happened, why it happened and which action follows.

Establish a reporting routine

Reporting date, responsibilities, commentary, action list and forecast update turn the BWA into a management process.

BWA Management Readiness Check

Answer ten questions and see immediately how close your BWA already is to a real management instrument.

10 questions for a first self-assessment

- Is your BWA usually available within 10 to 15 working days after month-end?

- Does it include prior-year or budget comparisons?

- Are material deviations commented in writing?

- Do you review gross margin and gross-margin percentage every month?

- Are unusual BWA lines checked against SuSa or account detail?

- Is there a connection to open items and liquidity planning?

- Is there a monthly management meeting around the BWA?

- Are actions from the BWA documented and tracked?

- Can the BWA be explained to a bank, board or investor without major additional work?

- Is there a forecast based on current development?

1. BWA exists, but is hardly used for steering

The BWA is received but not actively used.

Start the BWA Quick Check2. BWA is read, but not used consistently

Some figures are reviewed, but without a robust system.

Start the BWA Quick Check3. BWA is part of monthly steering

There are routines, commentary and first action logic.

Check BWA and SuSa together4. BWA is connected to reporting, forecast and actions

The BWA is part of a professional management system.

Explore DATEV/BWA reportingWhat a BWA should not be expected to do and what Momentum does not replace

A BWA is valuable, but it has limits. It does not replace tax advice, legal advice, annual financial statements, an audit or certified accounting output, a complete liquidity plan, a company valuation, a financing guarantee or management responsibility for decisions.

Momentum Advisory adds a management-oriented analysis layer to existing bookkeeping, tax-adviser and finance processes. We work on the basis of provided data and reports. The focus is interpretation, structuring, reporting, commentary and decision support, not tax or legal advice and not certified financial reporting.

Frequently asked questions about the German BWA report

What is a German BWA report?

A German BWA report is a monthly management accounting report generated from financial accounting data. It usually shows revenue, costs, gross profit and operating result, helping management teams assess current business performance.

What does BWA stand for?

BWA stands for “betriebswirtschaftliche Auswertung”, which means business management analysis or management accounting report. In practice, it usually refers to a monthly report from DATEV or another German accounting system.

How is a German BWA report structured?

A BWA report typically starts with revenue or total output, followed by material or goods costs, gross profit, cost blocks and result lines. For management-quality analysis, teams should also review trends, margins, cost ratios, accruals and plausibility against the trial balance, AR/AP and liquidity.

What is the difference between a BWA report and annual financial statements?

A BWA report is an interim monthly management report, while annual financial statements are prepared after the financial year and provide the formal legal and tax view. The BWA is faster and more useful for ongoing management decisions, but it is usually less final than annual accounts.

Is a BWA legally required in Germany?

The BWA is generally not a standalone statutory document in the same way as annual accounts. In practice, however, it is highly relevant for business steering, bank communication and financing preparation.

Who creates the BWA?

The BWA is often created by the tax adviser, the internal accounting team or a bookkeeping system. The key point is not only its creation, but the quality of the data basis and the interpretation that follows.

Is the BWA enough for bank discussions?

Often not on its own. Banks may request additional documents such as SuSa, annual accounts, open-item lists, liquidity planning, forecast or management commentary. The exact requirements depend on the situation.

What is the difference between BWA and SuSa?

The BWA is an aggregated management/accounting report. The SuSa shows account-level balances and movements. It helps explain the details behind BWA positions.

Why does the BWA not automatically show liquidity?

The BWA is primarily profit-oriented. Liquidity also depends on incoming payments, payment terms, receivables, payables, investments, loans, taxes and other cash effects.

When should a BWA be commented?

Whenever it is used for management decisions, financing, board reporting, investor discussions or significant business actions. Concise commentary significantly increases its usefulness.

What makes a BWA management-ready?

A management-ready BWA is timely, plausible, comparable, commented and connected to actions. It often also requires SuSa, open items, liquidity view, forecast and a clear KPI logic.

Turn your BWA into the start of a monthly management routine

If your BWA exists but is not yet consistently translated into steering, bank communication or forecast, the BWA Quick Check is the right entry point.

Heinrich Ruhwasser

Heinrich Ruhwasser is a seasoned entrepreneur and advisor with more than twenty years of experience in digital transformation, corporate strategy, and succession planning. As an expert in business growth, he has successfully guided a wide range of companies through complex transformation initiatives. His core area of expertise is increasing enterprise value, where he applies his deep knowledge to long-term planning and seamless business succession. Heinrich’s combination of visionary thinking and hands-on experience makes him a trusted advisor to executives and business owners.

How would you rate this article?

Did this article help, or is something missing? Your feedback goes straight into improving our articles.

We review every response and use it to improve both content and reading flow.

Related reading

How to Read a German BWA Report: A Practical Guide for Management Teams

How to read a German BWA report: practical 5-step sequence, key KPIs, warning signs and next steps with trial balance, open items and DATEV reporting.

E-Invoice Conversion: PDF, XRechnung, ZUGFeRD and structured data

Why safe e-invoice conversion starts with structured source data and why PDF-to-XRechnung is often risky.

E-Invoicing Formats in Europe: EN 16931, UBL, CII, Peppol, XRechnung, ZUGFeRD and KSeF

A practical overview of relevant European e-invoice formats, standards and national systems without thin country pages.