Short answer: do not read the BWA from top to bottom

Start with revenue and gross profit, then review people and overhead costs, interpret operating result afterwards, and validate critical anomalies against trial balance, open items or liquidity data. That turns the BWA from a list of numbers into a management signal.

How to read a BWA report: the 5-step sequence

This order helps management teams identify the most important signals without getting lost in individual accounts.

| Step | Question | Management signal |

|---|---|---|

| 1. Revenue and total output | Is performance developing as expected? | Demand, project status, seasonality or booking logic. |

| 2. Gross profit | Is enough margin left after direct costs? | Pricing quality, purchasing, service mix and project profitability. |

| 3. Personnel costs | Do staff costs, growth and productivity fit together? | Capacity, structural cost and scalability. |

| 4. EBITDA and operating result | Is the result operationally robust or distorted? | Earnings power, one-off effects and result quality. |

| 5. Trial balance, open items and liquidity | Does the BWA fit the account and cash logic? | Plausibility, open items, accruals and cash risks. |

How to Read a German BWA as a Management Report

A practical guide for managing directors, CFOs and controllers: compare trends and margins, test result quality, connect account detail, open items and liquidity, and assign the next action.

Accessible description and data

The infographic structures a German BWA review into five signals: revenue development, gross profit and margin, cost blocks, earnings quality and plausibility with SuSa, AR/AP and liquidity.

Understanding a BWA: which KPIs matter

A BWA does not automatically explain whether a month was good or bad. The important part is the connection between revenue, gross profit, cost structure, operating result and liquidity indicators.

For management teams, absolute values are rarely enough. Read ratios, trends and deviations: gross margin instead of revenue alone, personnel cost ratio instead of staff costs alone, operating margin instead of monthly profit alone. A single month becomes useful only when it is compared with prior month, prior year, plan or forecast.

For a broader introduction, read our full guide to the German BWA report.

BWA structure: which lines management should read

| Area | Meaning | Typical management question |

|---|---|---|

| Revenue and output | Economic performance recorded for the period. | Is growth real, sustainable and booked in the right period? |

| Materials and external services | Direct cost of delivery. | Is the service mix or purchasing situation changing? |

| Gross profit | Margin after direct costs. | Is enough contribution left for people, structure and profit? |

| People and overhead costs | Cost base that needs active steering. | Does the cost structure fit the current company size? |

| Result and commentary | Operating result, one-off effects and management interpretation. | Which deviation needs explanation or action? |

Typical warning signs when reading a BWA

Many warning signs look small at first. They become critical when they repeat or cannot be explained.

Revenue rises, gross profit falls

This may point to pricing pressure, project issues, discounts, purchasing topics or a changed service mix.

Profit rises, receivables rise faster

The BWA can look positive while liquidity and working capital already become strained.

Personnel costs jump without explanation

Missing accruals, bonuses, one-off payments or capacity issues should be reviewed.

One month looks unusually good or bad

Late bookings, one-off effects or period shifts can distort the management message.

BWA and trial balance: why the BWA alone is often not enough

The BWA summarizes result lines. The trial balance shows the account-level detail underneath. When the result needs explanation, BWA summary lines are often not enough.

Typical cases: The BWA shows profit, but receivables increase strongly. Revenue is high, but cash collections lag. Personnel costs look unusual because accruals are missing. The result is positive, but open items or liquidity point in another direction.

For these questions, the BWA + SuSa Check is the more useful next step.

BWA as a basis for company value and EBIT multiples

When a BWA is used for succession, sale preparation or financing, it should not only be read but tested for earnings quality. The next useful reference is calculating company value with formula, multiples and calculator: it shows how adjusted EBIT, revenue multiple and asset-based value form a value range.

DATEV BWA reporting: from export to management reporting

Many German subsidiaries and mid-market companies receive DATEV BWA, trial balance or open-item exports every month. The bottleneck is rarely the export itself. The harder part is repeatable interpretation: account logic, KPI mapping, plausibility checks, commentary and a format that management, banks or shareholders can actually use.

If you want to turn recurring DATEV data into a monthly report, DATEV BWA Reporting is the commercial next step after this guide.

Choose the next step

If you are working from a concrete BWA right now, start with the Quick Check. The other paths fit when you first want to structure values, validate them more deeply or build recurring reporting.

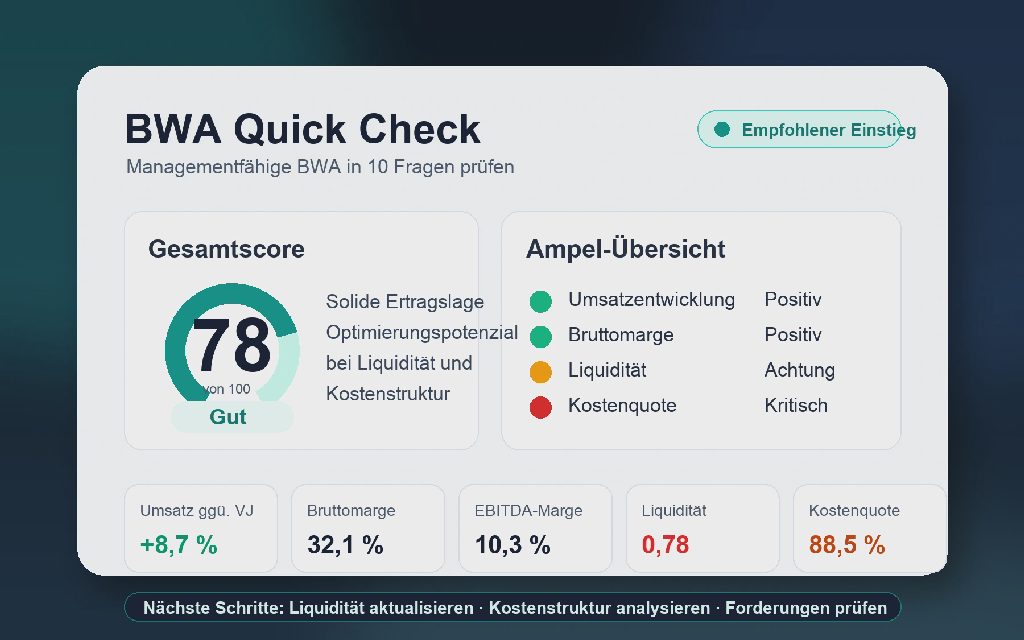

BWA Quick Check

The best starting point when you want to interpret current BWA values, prioritize warning signs and define the next management questions.

BWA Excel Template

For teams that first want to structure BWA values, understand sample figures or use a simple internal working file.

BWA + SuSa Check

When summary lines are not enough and account detail, open items, accruals or liquidity logic need to be checked.

DATEV BWA Reporting

When monthly DATEV exports should become a recurring management report with KPI logic and commentary.

Frequently asked questions about reading a German BWA

How do you read a German BWA report correctly?

Read a BWA report in a structured sequence: revenue development, gross profit and margin, cost blocks, earnings quality and plausibility. Do not only look at the current month; compare it with the previous month, prior year, budget and supporting data such as trial balance, AR/AP and liquidity.

Which KPIs matter most when reading a BWA report?

The most important KPIs are revenue development, gross profit, gross margin, personnel cost ratio, other cost blocks, EBITDA or operating result and earnings quality. The key question is whether these figures together provide a plausible picture of operating performance.

How do you read a DATEV BWA report?

A DATEV BWA report should not be read line by line only. Start with revenue and gross profit, then review cost blocks and results, and check unusual positions against trial balance, AR/AP and liquidity. This turns the DATEV export into a more reliable basis for management decisions.

What is the difference between BWA and SuSa?

The BWA summarizes result lines. The SuSa, or trial balance, shows account-level balances and helps validate anomalies in the BWA.

When is the BWA alone not enough?

When the numbers are used for banks, advisory boards, financing, M&A, restructuring or important management decisions, trial balance, open items, liquidity view and commentary should usually be added.

Heinrich Ruhwasser

Heinrich Ruhwasser is a seasoned entrepreneur and advisor with more than twenty years of experience in digital transformation, corporate strategy, and succession planning. As an expert in business growth, he has successfully guided a wide range of companies through complex transformation initiatives. His core area of expertise is increasing enterprise value, where he applies his deep knowledge to long-term planning and seamless business succession. Heinrich’s combination of visionary thinking and hands-on experience makes him a trusted advisor to executives and business owners.

How would you rate this article?

Did this article help, or is something missing? Your feedback goes straight into improving our articles.

We review every response and use it to improve both content and reading flow.

Related reading

BWA Report in Germany: From Accounting Export to Management Insight

A practical guide for management teams, CFOs and investors: how to read a German BWA report, interpret red flags, use SuSa detail and turn DATEV exports into monthly reporting.

E-Invoice Conversion: PDF, XRechnung, ZUGFeRD and structured data

Why safe e-invoice conversion starts with structured source data and why PDF-to-XRechnung is often risky.

E-Invoicing Formats in Europe: EN 16931, UBL, CII, Peppol, XRechnung, ZUGFeRD and KSeF

A practical overview of relevant European e-invoice formats, standards and national systems without thin country pages.